When assessing outsourcing arrangements, institutions and payment institutions shall determine whether an arrangement with a third party falls within the definition of outsourcing or does not constitute outsourcing.

This assessment should take into account whether the function (or part of it) outsourced to a service provider is performed by the service provider on a recurring or ongoing basis and whether that function (or part of it) would normally fall within the scope of functions that would or could realistically be performed by institutions or payment institutions, even if the institution or payment institution has not performed that function itself in the past.

What do you have to consider when differentiating between outsourcing and external procurement according to MaRisk? In the following article you will find answers to the following 14 questions regarding the delimitation of outsourcing and external procurement according to MaRisk:

- Which outsourced activities and processes are to be included according to § 25b KWG?

- No outsourcing within the meaning of § 25b KWG

- Requirements of the Audit Report Ordinance for reporting on outsourcing management

- Definition of outsourcing according to MaRisk

- Other institution-typical services – definition according to MaRisk

- Examples of: No outsourcing – Other outsourcing of services

- Does Depot A management with special funds constitute outsourcing?

- Are the risk ratios provided by KVGs to be classified as outsourcing?

- EBA guidelines with catalogue on services that do not constitute outsourcing

- Examples re: outsourcing – No classification as other third-party procurement

- Outsourcing management must be mapped in the strategy

- Outsourcing and concentration risks

- Minutes of the special meeting of the MaRisk expert committee on 15.03.2018 in Bonn (BaFin) Topic: Outsourcing

- Stricter requirements of the EBA Guidelines on outsourcing arrangements February 2019

Which audit criteria apply to the supervisory assessment of outsourcing controlling? Outsourcing: The EBA guidelines on outsourcing provide binding guidelines for the supervisory assessment. As part of their assessment, supervisors should consider the following 7 risks in particular:

- Operational risks associated with the outsourcing arrangement;

- reputational risks;

- the “step-in risk”, due to which the rescue of a service provider by the institution may be necessary, in the case of significant institutions;

- Concentration risks within the institution, including on a consolidated basis, arising from multiple outsourcing arrangements with a single service provider or closely related service providers or multiple outsourcing arrangements in the same business line;

- concentration risks at the sector level, e.g. where several institutions or payment institutions use a single service provider or a small group of service providers;

- the extent to which the outsourcing institution or payment institution controls the service provider or has the ability to influence its actions, the mitigation of risks that may be associated with a higher level of controls, and whether the service provider falls under the consolidated supervision of the group; and

conflicts of interest between the institution and the service provider. - Where concentration risks are identified, competent authorities should monitor the evolution of these risks and assess both their potential impact on other institutions and payment institutions and the stability of the financial market. Outsourcing: Guidelines on supervisory assessment require that competent authorities also inform the resolution authority of new potentially critical functions identified in the course of this assessment.

Institutions and payment institutions should, taking into account the principle of proportionality in accordance with Section 1, identify, assess, monitor and manage all risks to which they are or may be exposed as a result of arrangements with third parties. This shall be done irrespective of whether these arrangements are outsourcing arrangements or not.

The risks, in particular operational risks, of all arrangements with third parties, including those referred to in paragraphs 26 and 28, should be assessed in accordance with Section 12.2. of the EBA Guidelines on Outsourcing.

Institutions and payment institutions shall ensure that they comply with all the requirements laid down in Regulation (EU) 2016/679, including as regards third-party agreements and outsourcing arrangements.

As regards critical or essential functions, institutions and payment institutions shall ensure that the service provider has

- has the business reputation

- appropriate and sufficient skills,

- expertise,

- capacity and resources (e.g. human and financial resources, IT resources),

- organisational structure and

where applicable, the necessary regulatory authorisation(s) or registration(s) to perform the critical or essential function in a reliable and professional manner.

has.

This is the only way to ensure that the service provider is able to fulfil its obligations during the term of the draft contract.

Institutions and payment institutions should exercise due skill, care and diligence in monitoring and managing outsourcing arrangements.

Institutions shall regularly update their risk assessment and periodically report to the management body on the risks identified in relation to the outsourcing of critical or essential functions.

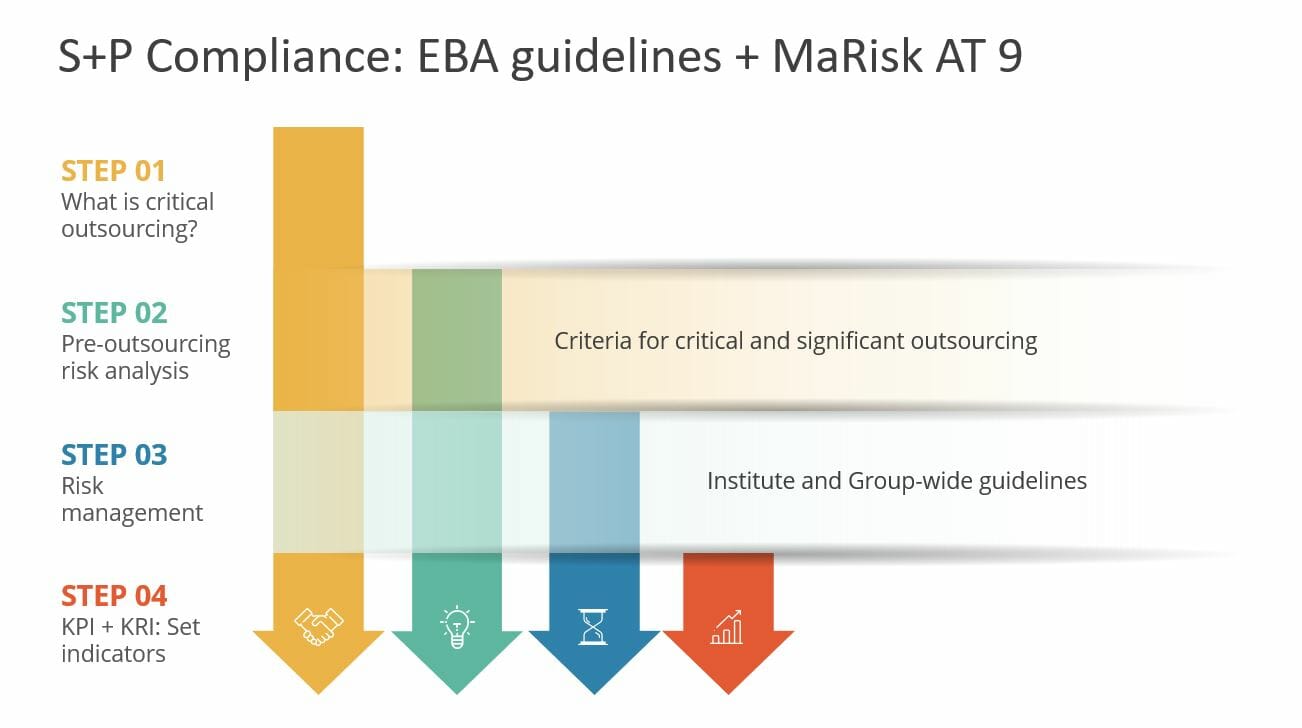

Institutions and payment institutions shall monitor and manage their internal concentration risks arising from outsourcing arrangements. The management can be carried out using the EBA Guidelines Outsourcing: Use of Key Performance Indicators.

New EBA Guidelines Outsourcing: What needs to be considered? The EBA Guidelines on Outsourcing also regulate the principle of proportionality. This principle applies to the compliance of institutions with the requirements for outsourcing as well as to the monitoring of compliance by supervisory authorities. For the application of the proportionality principle, the criteria developed by the EBA within the framework of the guidelines on internal governance can be used.

In addition, requirements are formulated for central outsourcing solutions within a group or a cross-guarantee system. Examples are a risk analysis, group-wide monitoring and control of outsourcing as well as an outsourcing register at group level. In this case, too, the individual institution remains responsible for compliance with the outsourced banking supervisory requirements. Thus, corresponding rights to information and reporting obligations must be established.

Institutions that have received an exemption from the supervisory authorities (“waiver”) only have to comply with the requirements at the level of the parent company (the central organisation).